10 steps to a successful company acquisition

Table of contents

Mergers and acquisitions can be risky, time-consuming, and complex. However, companies are improving their M&A approach to the point where, today, nearly 70% are reported as successful.

Successful deal-making involves many factors but a structured approach is the most crucial, binding all M&A activities into an effective, cohesive system. This article explores the 10 structural steps of a successful merger and acquisition process, along with valuable insights and best practices.

1. Creating an acquisition strategy

At the strategic planning stage, acquirers determine which M&A strategies best align with their long-term success goals.

| M&A strategy | Definition | Objectives |

| Horizontal | Acquiring direct competitors (businesses in the same industry) | Direct growth Greater market share Revenue synergies Cost synergies Customer bases Cross-selling and upselling opportunities |

| Vertical | Acquiring suppliers and distributors in the same industry | Strong supply chains Greater cost control Greater quality control Supply chain efficiencies |

| Concentric | Acquiring companies in complementary industries | New markets and product lines Cross-selling and upselling opportunities New revenue streams Technological advantage Strong innovative pipeline |

| Conglomerate | Acquiring companies in unrelated industries | Diversified revenues Diversified risks Access to new capital Greater market presence |

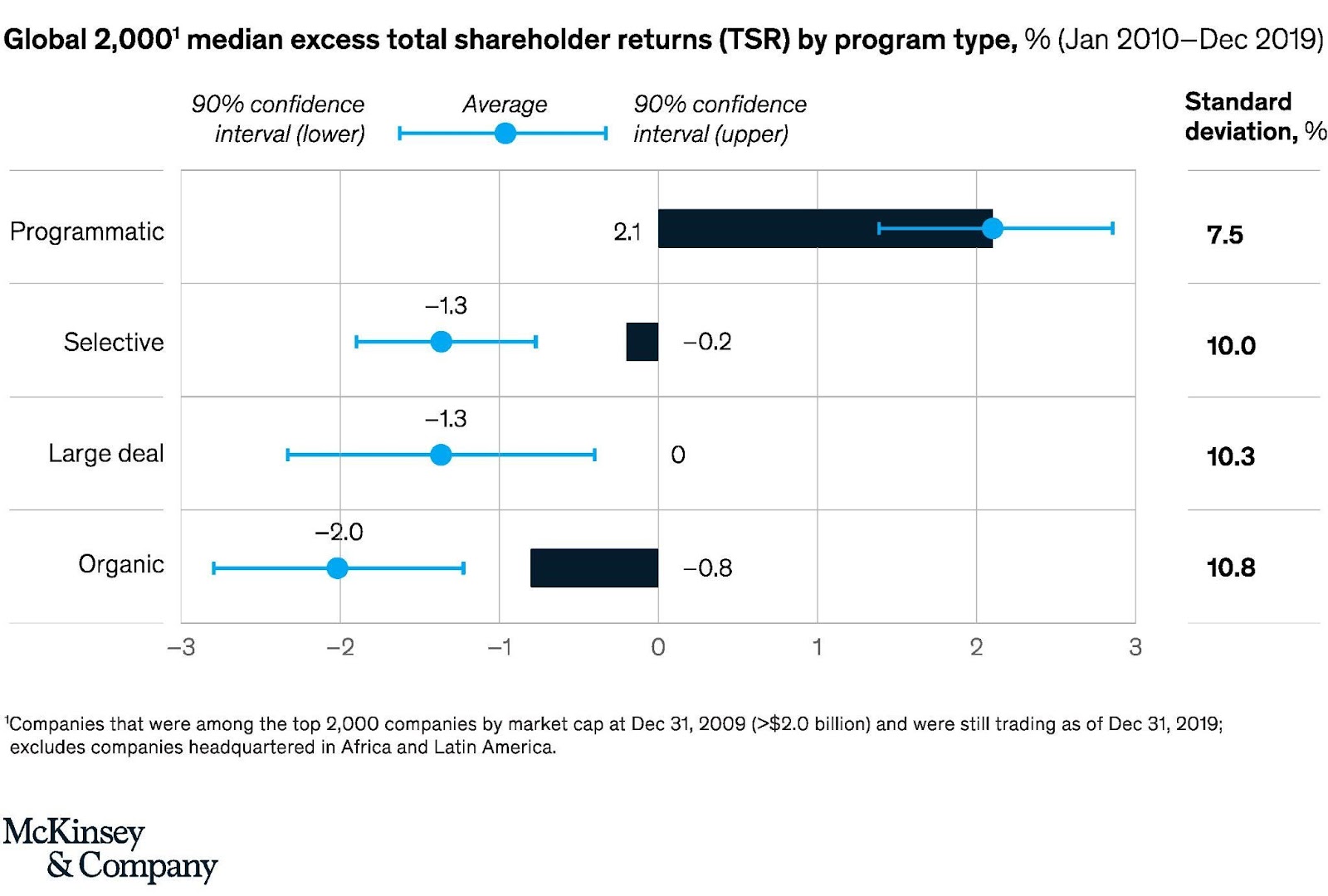

The importance of careful strategic planning can’t be overstated. Research shows that, historically, programmatic acquirers – those with well-defined business acquisition strategies – have a 2.1% median excess total shareholder returns (TRS), while other groups have zero or negative TRS.

Median TSR Performance by Program Type: Programmatic Strategies Lead

Source: McKinsey & Company

Aligning stakeholders during acquisition planning

M&A strategies are typically approved by board directors and shareholders. To have a greater chance of approval, executives should communicate the following elements of the strategy to board directors:

- Strategic rationale

This explains how the M&A strategy complements the company’s corporate goals — cost reduction, customer base acquisition, tech improvements and so on. - Value creation

Explains how the M&A strategy creates value for the company and its shareholders (revenue growth, competitive advantage or potential synergies). - Risk assessment

Explores how the M&A strategy accounts for existing risks, like regulatory concerns, financial risks, or potential integration challenges.

2. Building a list of potential target companies

It’s common for strategic acquirers and private equity firms to assess dozens of M&A opportunities before initiating in-depth due diligence. Acquirers begin building a list of target companies in attractive industry segments.

“The first step is to identify attractive industry verticals. That involves … looking at sectors where targets could support the core business…” Boston Consulting Group.

Common target search criteria include:

- Strategic fit

How well does the target business align with the acquirer’s M&A strategy — horizontal, vertical, concentric, or conglomerate? - Market position

How does the target’s market position benefit the acquirer? - Financial health

Is this target financially sustainable, and will this acquisition be profitable? - Synergy potential

Can this target create value beyond its standalone performance? - Growth potential

Can the target firm expand its revenue through products, geographies, or innovations?

3. Evaluating target companies

After initial target filtering, acquirers typically select a few attractive companies for detailed financial and operational screening. Typically, this involves three, broad steps:.

Preliminary financial review and valuation analysis

A preliminary financial analysis reviews the target company’s financial information and determines its worth (deal price). The following metrics are usually investigated:

- Profitability metrics

Profit margins, cash flows, EBITDA (Earnings Before Interest, Tax, Depreciation, Amortization), revenue growth rate, debt ratios, return on invested capital (ROIC). - Valuation multiples

Enterprise value to EBITDA (EV/EBITDA), price to earnings ratio (P/E), earnings per share (EPS), price to sales ratio (P/S), enterprise value to sales (EV/Sales).

Acquirers use these metrics in business valuation methods, including discounted cash flows (DCF), times-revenue, guideline transactions, historical earnings, for example. With public targets, acquirers use regulatory filings and reports, including annual reports (10-K), proxy statements, and current reports (8-K).

Yahoo Finance, SEC EDGAR, Google Finance, and Morningstar are useful resources when building these valuation models. For private targets, however, acquirers can use Pitchbook, Crunchbase, CB Insights, and other market intelligence tools.

Operational reviews

While preliminary operational reviews are typically limited, acquirers can collect considerable information from targets’ quarterly and annual reports, financial statements, press releases, and industry benchmarks. The following operational metrics are usually discussed during preliminary reviews:

- Customer acquisition cost (CAC)

- Operating margin

- Cost of goods sold (COGS)

- Production levels

- Upcoming product releases

- R&D expenditure

- Employee turnover

Red flags to watch in target companies

The following red flags may be revealed during company evaluations.

| Red flag | Potential issues |

| Volatile cash flows | Liquidity issues and difficulties in financing operations |

| Low profit margins | Low pricing power and operational inefficiencies |

| Declining customer retention | Customer service, product quality, and overpricing issues |

| Over-reliance on key customers or suppliers | High business disruption when key customers leave |

| High employee turnover | Management and operational issues |

| History of regulatory disputes | Ongoing and potential integration hurdles |

4. Initial contact with target companies

Acquirers typically approach targets through intermediaries like M&A advisory firms, investment bankers, or M&A lawyers, and sign non-disclosure agreements (NDAs). This approach helps to maintain a professional tone and signals that the acquirer is taking the acquisition seriously.

“In our experience, contacting a target through a financial advisor has an important signal function that the potential acquirer is serious and has initiated a process to prioritize and vet targets.” Mercer Capital.

Contacting sellers through intermediaries also helps them feel comfortable that sensitive information is being held confidentially (and not being used against the sell-side for market advantage).

5. Negotiating purchase price and terms

Deal parties typically sign a letter of intent (LOI) following the initial contact. Before signing LOI, an acquirer clearly outlines deal terms and discusses important considerations, including antitrust implications, tax considerations, employment laws, and licensing matters.

Negotiating prices, warranties, and representations is typically more challenging. Cautious buyers generally want lower valuations, while sellers pursue higher premiums.

“Two-thirds of buyers said a gap in valuation affected the ability to get deals done,” said Les Baird, Leader of Bain’s M&A practice in Bain M&A Report 2024

To bridge the valuation gap, acquirers use several tactics that meet sellers’ expectations while managing their own risks:

- Earnout

A part of the purchase price (10%–20%) is paid to the seller upon achieving certain milestones post-acquisition. - Seller note

A seller receives the payment in several parts over time rather than in one transfer. - Rollover equity payment

A seller receives the acquirer’s stock as part of the proceeds. - Spin-off

A method to resolve price disputes over specific parts of the seller’s business involves the seller ‘spinning off’ the disputed business, effectively excluding it from the current deal. - Partial purchase

An acquirer initially buys a partial stake in the seller’s business, with the agreement to purchase the rest at a future date.

6. Performing due diligence

Acquirers enter an in-depth due diligence phase when LOIs and necessary NDAs are signed. The due diligence process involves investigating the target company’s business functions:

- Finance

Financial statements, profit margins, working capital requirements, and recent financial transactions. The main goal is to evaluate financial risks and confirm or renegotiate the deal price. - Operations

Operations, supply chains, production processes, and internal controls. The main goal is to identify cost synergies. - Commerce

Sales performance, customer data, and revenue growth projections with the aim of identifying revenue synergies. - IT

Technology infrastructure and software systems to determine technological compatibility and scalability. - Cybersecurity

Data security controls, cybersecurity compliance, and data breach history with a view to assessing any data security risks. - Tax

Tax liabilities, tax filings, and tax implications. The main goal is to understand the tax benefits and develop the deal structure. - Human resources (HR)

Organizational structure, employee contracts, labor issues, incentives, and compensation structures. This will identify cultural clashes, directions for HR integration, and talent retention strategies. - Legal

Contracts, agreements, business licenses, legal disputes, and regulatory compliance issues in a bid to minimize legal liabilities post-acquisition.

| ALSO READ Review a detailed M&A due diligence checklist in our dedicated article. |

7. Structuring the target company acquisition deal

Buyers may initiate additional negotiations to account for uncovered due diligence details and price adjustments. These factors influence the deal structure, which defines the terms and conditions of the final purchase and sale agreement. Here are two of the most common deal structures.

Stock acquisition

An acquirer purchases the target company’s shares, gaining ownership of the entire business, including its assets and liabilities, while the acquired company remains a legal entity.

This straightforward structure means the acquirer avoids having to retitle individual assets and ensures the continuity of the target company’s contracts, licenses, and customer relationships. However, due to seller liabilities being assumed, this deal structure carries greater risks for the acquirer.

Asset acquisition

An acquirer purchases specific assets from the seller — business units, equipment, facilities, or intellectual property. It’s a partial, selective purchase where the acquirer assumes only certain liabilities. This structure allows for greater risk mitigation and provides the acquirer with greater tax benefits when depreciating and amortizing assets.

8. Finalizing contracts and regulatory filings

Upon negotiating the deal structure, deal parties sign a definitive purchase agreement with the following components:

- Purchase price

This section outlines the payment structure (all-stock, all-cash, or stock-and-cash) and financing options, like rollover equity payments or earnouts. - Warranties and representations

A list of assurances about the target’s conditions, including good standing, financial statements, and intellectual property rights. - Conditions to closing

This outlines specific conditions deal parties should meet before closing, like the resignation of the seller’s officers and regulatory approvals. - Covenants

Outlines the post-closing obligations of deal parties, including insurance policy retainment, public announcements, and non-solicitation and non-competition agreements. - Indemnification

Protects deal parties from the breach of warranties and representations, and outlines the indemnification terms.

If the transaction exceeds $119 million (the current threshold set by the Federal Trade Commission), regulatory approval under the Hart-Scott-Rodino Act is required.

It’s common for regulatory approvals to delay the pre-closing stage. In fact, about 40% of transactions took longer to close between 2018 and 2022 due to regulatory issues, according to Boston Consulting Group.

9. Deal closure

The parties involved actively work to meet closing conditions as the deal closes. Activities typically include obtaining regulatory and shareholder approvals, making payment transfers, and obtaining consent from customers, suppliers, and lenders.

A portion of the purchase price (10%-20%) may be reserved in an escrow account for 12 or 24 months, usually to protect the buyer from any breach of warranties and representations, and to manage the sellers’ working capital adjustments.

10. Post-merger integration phase

A post-merger integration office is formed before the deal closure to begin integration planning and prepare for the first operational day. An acquirer usually outlines the post-merger integration process checklist with key activities for various business functions.

These activities are time-bound and allocated to Day 1 (the first operational day post-close), the first 30–90 days, and 90+ days. Here are some key areas to focus on during post-merger integration.

Cultural alignment

Acquirers that address cultural integration early have 50% higher chances of meeting and exceeding synergy goals. That can be achieved through hard (such as financial bonuses) and soft (such as employee recognition) incentives for cultural adoption, high leadership involvement, early integration of key teams, and open communications.

Business continuity

Organizations can take various approaches to business continuity, from shifting crucial migration processes to off-peak hours to investing heavily in talent retention programs. Successful organizations also commonly use digital solutions to automate and accelerate integration processes.

System integration

Acquiring companies address system integrations early. However, because the integration pace differentiates across business functions, IT systems are integrated gradually. Generally, financial systems are integrated first, while research and development (R&D) systems are integrated later.

How Ideals VDR supports key stages of the acquisition process

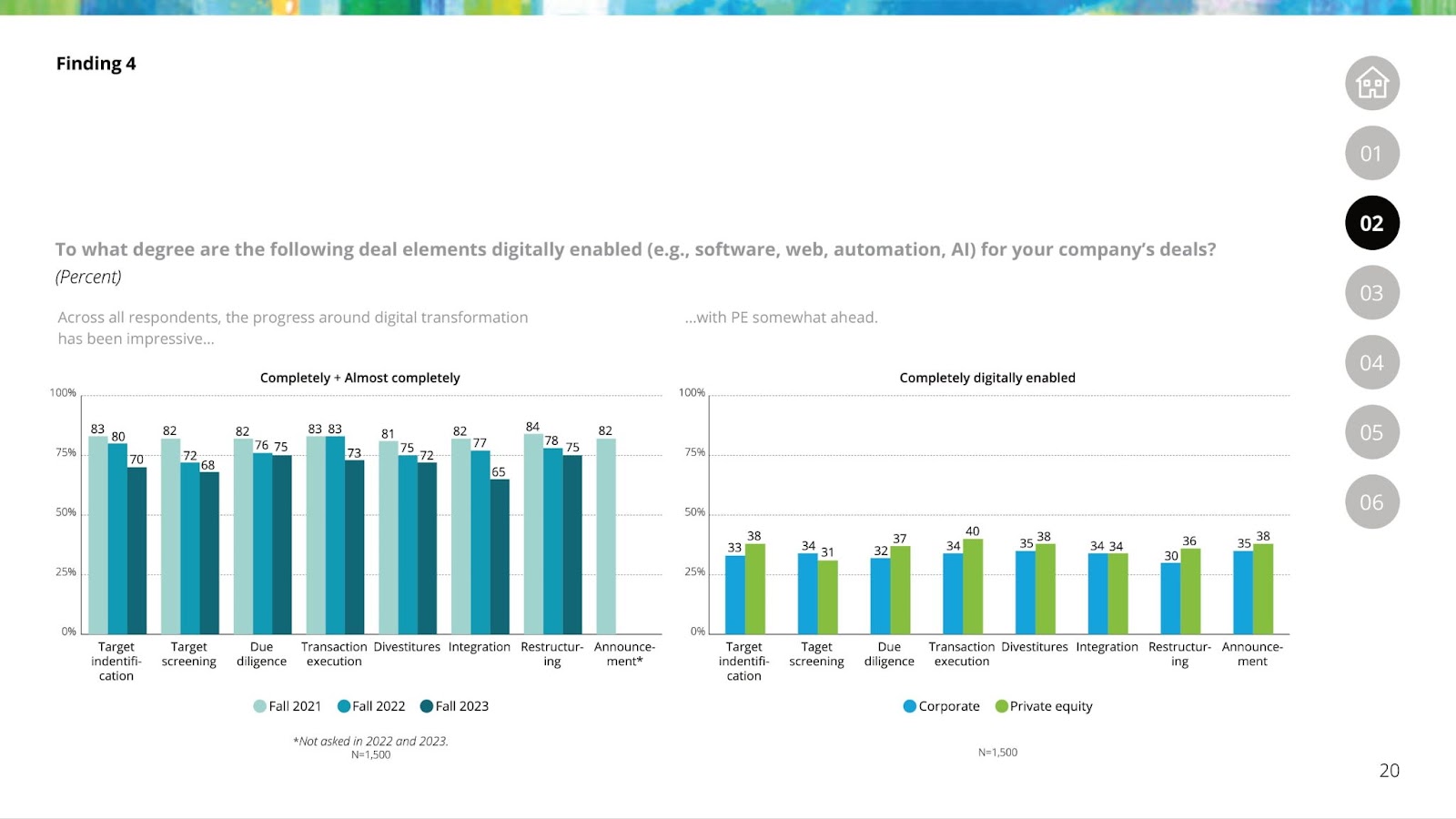

In today’s fast-paced M&A landscape, over 70% of acquirers have completely or almost completely embraced automation and AI.

Source: Deloitte 2024 M&A Trends Survey

Ideals Virtual Data Room (VDR) is a perfect deal automation solution to streamline your acquisition process, from strategy development to post-merger integration.

Designed for efficiency and security, Ideals delivers the following benefits to dealmakers:

- Efficient document management

Import entire folder structures, connect to external storage, use AI-powered data search, auto-convert files, and collaborate efficiently on both desktop and mobile devices. - Frictionless collaboration

Use advanced Q&A workflows with approver roles, share private and public notes, set up FAQs, and track user engagement with granular audit trails. - Superb data protection

Safeguard deals with eight levels of access permissions, AI-powered redaction, and information rights management security. - Premium support

Benefit from premium data room management services, 24/7 live support in more than 10 languages, dedicated success managers, and live data room training.

The bottom line

- A typical company acquisition entails strategic planning, target screening, initial negotiations, due diligence, deal structure development, deal closing, and post-merger integration.

- Identifying which M&A strategy best aligns with your business strategy is key to successful target sourcing and overall M&A success.

- Post-merger integration should heavily emphasize cultural alignment, talent retention, business continuity, and phased integration of IT systems.

- Virtual data rooms deliver exceptional capabilities in collaboration, data management, and cybersecurity at all stages of the acquisition process.

FAQ

A merger and acquisition is when one company (acquiring company) purchases and merges with another (target company) to realize its business goals, including market expansion, cost reduction, or technological advantage. The two companies merge and a new legal entity is formed.

The 10 steps in the acquisition process are strategic planning, target list building, target evaluation, initial contact, initial negotiations, due diligence, deal structuring, contract finalization, deal closure, and post-merger integration.

Post-merger integration (PMI) covers financials, commerce, operations, human resources, IT systems, logistics, procurement, research and development. PMI emphasizes business continuity, talent retention, and phased system integrations.

A business valuation is when an acquiring company determines the target company’s worth, while due diligence deeply investigates the target company’s business functions to confirm or renegotiate the valuation.